A lot of “smart” investors are claiming cryptocurrency miners face diminishing returns. Do so at your peril. There will undoubtedly be layers of winners in crypto, but miners will be much bigger for much longer than most people think.

But my research has convinced me that public companies in the cryptocurrency mining space will have a fabulous 2018.

So I am continuing to accumulate HIVE Blockchain (HIVE-TSXv) in the open market—even at $3/share. I bought stock in HIVE when it was private, then again in the first week under $1.

I have also bought into a private miner about to go public in January – DMG Blockchain (www.dmgblockchain.com).

DMG has executives from Bitfury (the world’s 2nd largest bitcoin mining and blockchain company), Cisco Systems, and PWC. They plan to be a fully diversified blockchain software and bitcoin company. Operations will include industrial bitcoin mining in Canada and offering mining as a service (Maas).

The big news of course, is reports coming out of China that some miners are being forced to shut down.

It’s all rumours and hearsay of course.

There is no official announcement from the Chinese government. And the South China Morning Post has an article that individuals are still free to mine cryptocurrencies.

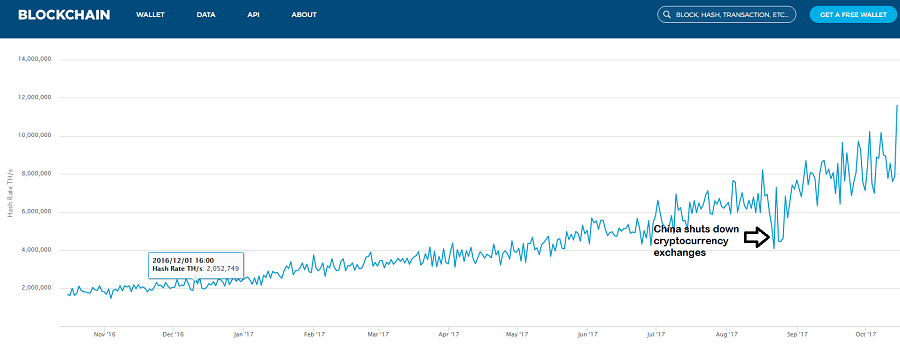

This chart measures the total hashing power of the miners on the Bitcoin network.

The Hash Rate is the speed at which a computer is completing the mathematical puzzle that will allow it to complete a transaction. A higher hash rate is better when mining as it increases your opportunity of finding the next block and receiving a reward.

At first glance, it looks like all is well, you are seeing increased hash rate – more servers – being added to the Bitcoin network.

The sudden decline in hash rate during September is easily explained by the China crackdown in September and the hash rate spikes up again.

But what is interesting is that hash is not being added as quickly as it should be. Let me explain.

The price of Bitcoin is what motivates people/companies to buy servers to act as miners to the Bitcoin network. The current price of Bitcoin is north of $5500 US and currently 12.5 Bitcoins are mined every nine minutes.

So monthly revenue for Bitcoin miners in October = Days in month (31) x Hours in day (24) x Minutes in a hour divided by 9 (6.67) times number of Bitcoins produced every nine minutes (12.5) x price of Bitcoin $5500 = $341 million US.

For the sake of simplicity, I’m not taking into account transaction fees even though they can be quite substantial (as high as a million dollars a day).

In November of 2016 the price of Bitcoin was $640. If we plug in that number into the formula then we get approximately $40 million for monthly revenue in November 2016

Revenue for Bitcoin miners has grown year-over-year at 1600%.

However, the investment in servers has not kept up. In November 2016 the total amount of computing on the Bitcoin network was 1.7 million T/hs per second. The hashrate by the end of October should be 12 million T/hs per second. That’s “only” an increase of 700%.

After a full year of running a Bitcoin mining server or “rig”, your gross monthly revenue would have increased by 226%.

This is almost unbelievable, so I will put it another way.

Year-over-year, there are 7 times as many Bitcoin miners, or the Bitcoin mining community computing power has gone up by a factor of 7.

But revenue has climbed 16 times over.

Therefore each Bitcoin miner is making 2.25 times as much money now as opposed to a year ago, with no additional capital investment.

This is truly mind-boggling because in theory as a market gets bigger, profitability should go down. But it’s going up.

Something is very fishy (in a good way for me) and even though I don’t have airtight case to pin it all on the Chinese political situation, it still…. looks that way.

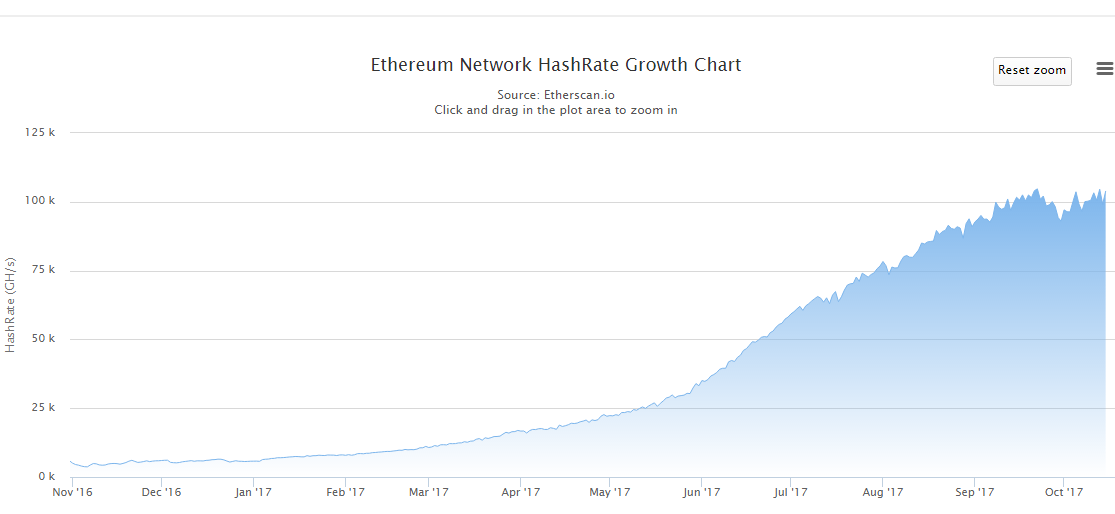

The story of Ethereum is similar.

For mining Bitcoin, you need to use special custom-designed chips called Application-specific integrated circuit (ASIC) chips.

It’s tough to get a hold of those chips and the big Bitcoin miners get first crack at the “rigs.” If you are retail, it’s virtually impossible to buy a Bitcoin mining rig unless it’s second-hand.

But for mining Ether, it’s much easier to get your hands on the graphics cards from Radeon (owned by ATI) and Nvidia that can be used for mining.

Therefore, it follows you would see a massive bump in computing power over the last year for Ethereum, as there should be less of a bottleneck from chip suppliers:

At first glance, the growth in hashing power looks impressive. The hash rate has gone from 5,700 GH/s at beginning of November 2016 to just under 100 GH/s at present – that’s an increase of 1750%.

However, in same period, the price of Ether has gone from $12.50 to $330 – an increase of 2640%.

Doing some quick calculation, the profitability of a Ethereum mining rig has gone up 50% in the last year.

That is to say, a rig generating $1000 a month in November of 2016, is now $1500 a month.

This is not including transactions fees collected by miners, which are currently running at at $600,000 a day.

What Does It All Mean?

I can only think of two possible reasons why cryptocurrency mining has become more – not less – profitable over the past year.

One would be a chip shortage i.e. chip makers and graphics card supplies can’t keep up with demand. This is good news for my thesis as wholesale buyers of equipment aka big companies will be first in line to get the gear and retail will continue to get the dregs.

The second reason would be the investment climate in China, currently home to 70-80% of the world’s cryptocurrency miners.

It’s not a stretch to say the investment climate in China is lousy, and even if the government doesn’t ban cryptocurrency mining outright, I think everybody agrees that opening up new data centres would be…risky.

Cryptocurrency Miners Are Moving Out of China and Into the Public Markets

One big reason why cryptocurrencies miners are in China is access to cheap electricity: it’s 8 cents per kilowatt-hour in China. But in Canada it’s only 10 cents or 2 cents higher according to some sources, but other sources put the industrial price below eight cents or even cheaper than China.

Note that HIVE has two centres in Iceland where geothermal energy drives the rate down (for industrial users) to a rumoured 3 cents a kilowatt hour.

Therefore, assume that investment capital for cryptocurrency mining is going elsewhere i.e. not China.Canada and any other country with good industrial pricing for electricity is a reasonable bet.With regard to Canada, it can’t hurt there is a huge Chinese diaspora in Vancouver. There are two direct flights from Beijing to Vancouver a day. Vancouver is home to the TSX venture stock exchange, an exchange with a reputation for allowing…speculative industries to raise public capital.It all adds up. Or it adds up enough for me to put more of my own money into the pot.

Guessing the Future Market Capitalization of Cryptocurrency Miners.

Obviously, we must make assumptions here but it helps greatly we don’t have to guess at all about the current revenue of the cryptocurrency industry.

Bitcoin miners are making $341 million a month in mining and an additional $30 million a month in transaction fees. Assuming the price of Bitcoin stays at $5500 (yes that’s a big assumption), then annual revenue is $4.45 billion.

Ethereum miners are making $2.55 billon US a year plus transaction fees of at least $200 million for a total of $2.75 billion(again assuming price stays constant).

That’s a total of $7.2 billion a year in revenue. What should be the market capitalization of the cryptocurrency industry?

For the sake of comparison, there are 46 public-listed silver mining companies in the world. The market cap of the top ten sliver companies is $18.94 US billion. The entire revenue of the silver industry is $15 billion US for a market-cap-to-revenue ratio of 0.8.

Now I would argue that cryptocurrency miners deserve a market cap to revenue ratio of least double that, or 1.6, because if you were an investor with $10 million to spend, would you invest in opening a silver mine or a bitcoin data centre?

I think a ratio of 1.6 is stupidly low, but let’s go with that number for argument’s sake. Thus, we arrive at a market capitalization of $11.50 billion US for the cryptocurrency mining sector by end of 2018.

Now we must do a second big assumption: In the next year, what percentage of the crypto-mining sector will go public? Will it be 100%, 50%, or even as low as 20%?

Even if we take the lowest assumption, that still means the market capitalization of $2.3 billion US for all publicly-listed cryptocurrency miners.

The current market cap of HIVE is $593 million US. When DMG comes to market in November it will have 77 million shares out for approximate market cap of $77 million US (that’s a guess based on HIVE’s first day performance).

That’s a total of $670 million cap US. Therefore, both HIVE and DMG have to grow by 345% next year to make it to $2.3 billon or there has to be new public companies floated in the market space. I am betting it will be a combination of both.

Conclusion

It is a given that some of my forecasts are wrong.

It is quite possible that ALL of my forecasts and assumptions are wrong.

But for me to lose money, most if not all of my forecasts have to wrong by an ORDER OF MAGNITUDE.

It’s not enough to poke holes in these assumptions; you must make a hole big enough that a Ford F150 can drive through it, before I start to think I might lose money investing in this sector.

If anything, my numbers are too conservative.

For example, if the price of Ethereum averages $500 USD for all of 2018 and HIVE grabs 30% market share (this is very do-able as HIVE is backed by Genesis Mining) then you get an absurd number of $1.25 billion US a year revenue for HIVE for a market cap of $2.25 billon US or $9 a share.

Ross

Note: I am long HIVE